Le Tour de Finance – a winner again

By Spectrum IFA

This article is published on: 1st June 2014

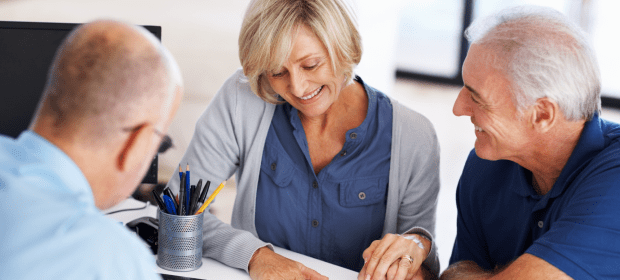

Last week, my colleague Rob & I presented at two of the South West France venues of Le Tour de Finance. This is a tour that travels around France, where we bring ‘experts to expats’. Now in its fifth year and due to the popularity of ‘Le Tour’, the events take place around the country in both spring and autumn.

Rob and I did a ‘double act’ and gave a presentation on The Spectrum IFA Group, which covered our processes and the products and services that we provide to clients, as well as highlighting the importance of our independence and how we are regulated in France by the French authorities. We also discussed client concerns (tax-efficiency, inheritance tax planning, securing pensions, protection of capital and continuing issues about the security of banks in the Eurozone).

SEB Life International and Prudential International presented on the topic of assurance vie, explaining the tax-efficiency of this type of investment, both personal and for inheritance planning. Each of the companies outlined the unique features of their own products and it could be seen that the products complement each other, one or the other being more suited to a client, depending upon attitude to investment risk.

The Standard Bank provided details of its structured product offerings that are currently available. There are different terms available and there is an element of linking to stock market performance with this type of investment, but all provide a guarantee that at least the original capital invested will be returned at the maturity date. For our clients who invest in these Standard Bank products, when used in conjunction with a particular life company wrapper, the clients benefit from an extra bonus, which is provided in addition to the capital guarantee.

Currencies Direct presented the various options open to clients who wish to exchange currency, whether this is for regular payments or for ad-hoc exchanges perhaps for larger purchases, for example for property. It was very interesting to see how much could be saved by using Currencies Direct, rather than a retail bank. Unexpectedly, as the Sterling Euro exchange rate jumped by more than a Euro between one day and the next over the two days when Rob and I were at Le Tour, currency exchange proved to be more topical than any of us were expecting.

Exclusive Healthcare Insurance presented on the range of products that they can offer clients. This included a range of seven different mutuelle plans that top-up the basic French health cover, which are designed to meet the needs of the different income groups of French residents and the variation in medical costs from region to region. Like all mutuelle insurance in France, there are no underwriting conditions and pre-existing conditions are covered. The company also outlined a different product that provides full private medical insurance, but which is subject to underwriting conditions. However, since the UK will stop issuing Certificates S1 to early retirees from July this year (i.e. for those who are not receiving UK State pensions), this might be a viable option for those who may be affected.

There was a presentation on French succession planning from Heslop & Platt, which is a firm of UK solicitors that are specialists in French law. As many of our clients maintain a connection with their former home country, the importance of ensuring that there is no conflict existing between the wills made in the different jurisdictions was highlighted. In addition, the forthcoming EU rules on succession were outlined and it could be seen that there would still be a need in France for inheritance planning the ‘French way’ to avoid the French inheritance taxes that will still exist even when the EU rules are in operation from August 2015.

New to Le Tour this year was PetersonSims, a firm of chartered accountants based in France, which also specialises in expatriate tax issues. A presentation from their Tax Director demonstrated how much money they could save clients, just by making sure that French tax returns are completed correctly and relief from double taxation is obtained.

If you did not make it this time to Le Tour de Finance, keep in mind the next local events which will take towards the end of June. On the other hand, if you would like to have a confidential discussion now on your financial situation, please contact me by telephone on 04 68 20 30 17 or by e-mail at daphne.foulkes@spectrum-ifa.com.

The above outline is provided for information purposes only and does not constitute advice or a recommendation from The Spectrum IFA Group to take any particular action on the subject of investment of financial assets or the mitigation of taxes.

The Spectrum IFA Group advisers do not charge any fees directly to clients for their time or for advice given, as can be seen from our Client Charter

Capital Gains Tax and the Expat Property Owner

By Spectrum IFA

This article is published on: 28th May 2014

You have realised your dream, bought a property in France, perhaps as a holiday home to start with but now you have moved here, maybe to work, or perhaps you have retired. The big question is what to do with your property or properties in the UK?

When moving to a new country many people are a little nervous about letting go of their old one, rightly so after all holidaying is one thing, but living in a foreign country quite another. So often people keep their property in the UK, for a while at least, however this can have Capital Gains Tax (CGT) implications on a future sale.

A tax treaty signed between France and the UK which became operative on 1st January 2010, meaning that for former UK residents now resident in France, they are liable for french CGT on the future sale of any property including your former main residence. However no liability will apply in the UK.

Main Residence

If you sell your UK home when you move to France or within a relatively short space of time (usually within a year) then no CGT will be payable in either France or the UK. If however, you hold into it for a while ( then or rent it out) then you will pay CGT on it in France just like any other maison secondaire, with no allowance being made for the fact that it was your main home for a period of time.

Buy to let

If you sell your UK buy to let property when you move to France rather than at a later date then you will pay UK CGT. To work out how much tax you will have to pay, take the selling price of the property, then deduct the buying price. You can deduct the costs of buying and selling, e.g. solicitor’s fees, stamp duty, estate agents fees, advertising etc. You can also deduct the cost of

improvements to the property but not routine maintenance and repairs. There is also an annual exemption allowance (£11,000 for 2014/2015 tax year). CGT rates are 18% or 28% for higher rate tax payers. HMRC website provides a step by step guide.

Any buy to let properties that you own in the UK and subsequently sell after you become a french resident will be liable to French CGT.

Ownership

An important point to note, if you are married, but your UK property is only in one person’s name, it may be sensible to transfer the property into joint names prior to any sale to reduce any potential UK CGT liability. There is no CGT payable between spouses/civil partners and the CGT calculation on sale will be based on the original purchase price for both parties.

In France Gift Tax applies between spouses and applies to gifts made in the previous 15 years so it is sensible to take advice from a professional before taking any action.

French CGT

Like UK CGT, you start with the sale price and deduct the purchase price plus any associated buying and selling costs and costs of improvements (but not repairs or DIY, invoices need to be provided from registered builders etc). If you have owned the property for more than five years the notaire can apply an allowance of 15% of the original purchase price of the property – even if you haven’t done any work!

For EEA residents the starting rate for french CGT is 19% plus 15.5% social charges however these start to reduce on a sliding scale from year 6 of ownership onwards. After a full 22 years have passed the CGT reduces to nil, however it is 30 years before the social charges reduce to nil. Additional charges apply for gains above 50,000 euros.

Working out when, where and how much Capital Gains Tax you should be paying can be quite a headache and the best thing to do is take advice from a professional.

This article is for information only and should not be considered as advice and is based on current legislation. 25/05/2014.

Should I use a Financial Adviser?

By Peter Brooke

This article is published on: 24th May 2014

Creating a financial plan is NOT a complicated thing to do; it is an audit of where you are today, financially, and where you want to be at different stage of your life. This requires creating a list of what you have, earn, own and owe and agree with yourself to put something aside to cover different goals for the future.

If we don’t have goals in life there is probably little point in getting up in the mornings; unfortunately most things cost money and so having financial goals is also an important part of life. Money doesn’t buy happiness, as we all know, but it does buy some choice and, to some extent, some freedom. I have met yacht crew who have worked for 20 years without implementing a financial plan and want to leave yachting; as they have no pensions and minimal savings or investments they are left with a simple choice… live on very little or keep on working… I see this as a loss of freedom, and so do they.

So we can agree that having a financial plan, however simple, is a very important thing to have but why have (and pay) someone to help you bring this together?

The process – though doing a plan is quite simple a financial adviser will ensure that all areas are discussed and re-examined so nothing is left out. All of the horrible ‘what if’ questions should be covered:

Implementation – a good adviser will have access to thousands of products from to use with different clients who have different needs. The more choice available the more assistance you will need in choosing the best ones, but also the more independent the advice will be. A small advisory firm is likely to have only a few products to choose from and so will display less independence.

Professionalism – if we are ill we go to a doctor; they have qualifications to diagnose our problems and help to put together a plan to make us better. Likewise with a lawyer. A financial adviser should also have qualifications in his or her trade too. Some advisers also specialise in certain areas, like investment or protection etc.

Regulation – like a Doctor or lawyer a financial adviser will be regulated by a government body and will have to display a certain competency and have insurance in order to practice.

Knowledge – qualifications don’t guarantee knowledge, a good adviser should continually improve their knowledge and should be able to prove this through their ability to explain complex issues.

Humanity and perspective – most importantly you need to trust your adviser, this person or firm should be your trusted adviser for most of your life; they need to be able to empathise with the different situations you will find yourself in over the years. They should be able to draw on experience from other clients to help solve issues you face too; they should be able to offer perspective on the decisions you make.

This last point is the hardest to prove and is probably best achieved through a combination of your own ‘gut instinct’ and referrals from friends and colleagues. Do your own research on the all of the above factors, ask around and keep asking around until you have a short list of advisers to meet… then follow your own feelings as to whether you can trust them; the relationship should be a long term one and you will end up telling them a lot of very personal information over time.

This article is for information only and should not be considered as advice.

This article appeared on the FEIFA website. The Spectrum IFA Group is a member of FEIFA. (The European Federation of Financial Advisers and Financial Intermediaries)

Buying Property in France

By Peter Brooke

This article is published on: 23rd May 2014

Buying property is one of the most major investments we make in our lives. For yacht crew, it’s rarely for a primary residence, which makes the considerations for buying a little different.

Location will always come first, but when using property as an investment, yield should be a very close second. This is the net annual rental income (after all costs) divided by the value. One of the biggest reasons why property is considered the best investment is because it’s possible to leverage, or borrow, to buy it, especially when interest rates are low. For example, if you buy property for €200,000, and it gives a rental income of €8,000 per year, a four-percent yield is realized. If you only invested €40,000 and borrowed the remainder at three percent interest, then you immediately double your yield to eight percent. This is a compelling reason not to invest all your capital into a property. Even if interest rates are higher, it may still make sense, as it’s often possible to offset the interest against rental profits to reduce income tax.

Buying property in France is very popular amongst yacht crew, especially near the yachting centers of the Côte d’Azur. This is because the property can be a great escape in the winter when the yacht is in port or the yard, and also gives a great seasonal rental yield in the summer, the time when crew are hard at work.

These areas also are very sought after and selling a property is rarely difficult. The costs of buying in France are quite high; government taxes and notary (legal) fees total approximately 7.5 percent of the purchase price, and agent fees (when you sell) can be five or six percent. This means 13 percent growth on the property is necessary to make any capital profit, which is why property should be seen as a long-term investment and why rental yield is important. Annual taxes also apply and vary depending on where the property is located and its size. Borrowing in France is still possible for yacht crew, although it’s getting a little harder as banks tighten their rules. Generally, crew can borrow 75 (sometimes 80) percent of the purchase price. This means you need approximately 32.5 percent deposit (including notary fees) to start your property portfolio.

French lending laws allow you to be up to one-third of your income in debt, so if you earn €3,000 per month, you cannot spend more than €1,000 on your debt repayments. Over 20 years at three percent, €1,000 per month equates to a loan around €185,000. For tax-resident yacht crew (in France or any other country), the loan-to-value can often be higher as tax documents make banks feel more comfortable about lending. Any rental income is taxable in France, whether you are resident or not, and capital gains tax and inheritance tax will be initially liable in France, too.

There are many considerations when buying property, so seek good, qualified advice especially if it’s part of an overall plan; a mortgage broker should be able to find the best terms for you, often at no cost.

Le Tour de Finance in France

By Spectrum IFA

This article is published on: 22nd May 2014

After a hugely successful run of events in Italy and Spain, Le Tour de Finance has come home to France for a run of 9 events throughout the country.

The first 5 legs of le Tour are taking place from 20th – 23rd May. The final 4 events are taking place towards the end of June from 17th – 20th.

These informal events are a great opportunity for expats of all ages to get those unanswered financial questions clarified in plain English.

The range of professional speakers is varied and will cover a multitude of subjects from; Pensions & QROPS, Currency Exchange, French Wills, Tax Efficient Investing, Estate Planning & Tax Advice in France.

These sessions are free, you’ll get to meet other expats in your area and can finish the morning with a complimentary buffet.

For further details on future events please click here.

Reflections on the recent ‘French Property Exhibition’ in the UK

By Spectrum IFA

This article is published on: 16th May 2014

For the first time The Spectrum IFA Group participated in this regular UK event on the 9th – 10th May as part of Le Tour De Finance Roadshow (www.letourdefinance.com)

For the first time The Spectrum IFA Group participated in this regular UK event on the 9th – 10th May as part of Le Tour De Finance Roadshow (www.letourdefinance.com)

Organised specifically for those UK residents looking to purchase property in France as either a second home or for a permanent move, the event brings together a range of experts to help delegates further their plans & aspirations.

Amanda Johnson & Bérangère Chabenat represented The Spectrum IFA Group this year, with the aim of providing attendees information on financial planning & mortgages which would assist potential buyers in their longer term financial situation.

The event was very well attended & many delegates took the opportunity to enter our free prize draw, the winner receiving a hamper containing some of the Loire Valley’s excellent sparkling wines, champagne flutes in which to enjoy it & local confiture de vin.

Le Tour de Finance was of great interest to many attendees, with eight people signing up to attend the events in June & several others expressing a wish to be informed of future seminars.

After a full day of manning the stand, Amanda & Bérangère found the opportunity to network with other exhibitors in the evenings over a glass of wine.

A good time was had by all.

Click here for information on Le Tour de Finance events during May and June 2014

Who is “Ask Amanda?”

By Amanda Johnson

This article is published on: 15th May 2014

As it has been over 2 years since I introduced myself to Deux Sevres Magazine readers, I thought a reminder of who I am would be helpful:

Along with drawing on the resources of The Spectrum IFA Group, one of Europe’s leading independent intermediaries, I have 25 years of experience in financial services.

For over 15 years I have specialised in personal financial planning. Whilst in the UK I worked for several UK high street banks as a financial advisor, attaining the following Certificate for Financial Advisers (CeFA®) qualifications: C.E.F.A I, C.E.F.A II, C.E.F.A III & CEMAP

After a permanent move to France in 2006, I have been addressing the unique financial planning needs of expatriates and those with cross-border interests. I have a detailed knowledge of the French rules & regulations for tax efficient investments, pension organisation, Inheritance planning & French mortgages.

In making recommendations we have access to some of the world’s most respected international banking, investment management and insurance institutions, bringing customers a widespread range of services.

There are no consulting fees for providing you with advice or ongoing service. Our Client Charter outlines how we work and what you can expect from us. Please do not hesitate to ask for a copy of this.

Whether you want to register for our newsletter, attend one of our upcoming road shows (June 17th & 19th) or speak to me directly, please call or email me on the contacts below & I will be glad to help you. We do not charge for reviews, reports or recommendations we provide.

Amanda Johnson tel : 05 49 98 97 46 or 06 73 27 25 43 e-mail : amanda.johnson@spectrum-ifa.com web: https://spectrum-ifa.com/amanda-johnson

Tax Returns, Pensions & Seminars

By Spectrum IFA

This article is published on: 28th April 2014

What do the above have in common? Well nothing really except they are all topical now! Let’s start with tax returns ……..

I was really surprised to receive the French tax forms so early this year and then I realised why. The date for submission of paper returns has been brought forward to 20th May or if you submit your declaration over the net, then you have until 27th May to do this. Does this mean that we are going to get our tax demands a week or two earlier this year and perhaps with an earlier deadline date for payment? Well I guess that we will just have to wait and see.

No-one should ever try to second guess the Fisc or think that they can out-manoeuvre this government department. I hear some interesting stories of people being contacted and questioned about why they are not registered in the French tax system. You would be amazed at what is used to check – telephone bills, utility bills, etc., etc. How long will it be before our use of cash machines and our bank and credit card transactions in shops might be used to verify how much time we spend in France? Scary thought and actually they probably don’t need to go that far, as we can be tracked through our mobile phones and probably also our internet use.

Are you convinced now to register in the system? You’re still not sure if you are resident? OK, call me and with just a few questions, I will be able to tell you.

For those of you completing French income tax returns, don’t forget to include a list of foreign bank accounts and life assurance policies. You don’t have to declare amounts (unless you are subject to wealth tax), only the existence of the accounts and policies. If you don’t, the penalty is at least €1,500 per undisclosed account/policy or €10,000 if the bank account is in one of those uncooperative States or territories that have not concluded an agreement with France to exchange information. So even if it is an account that does not pay interest and there is very little in the account, declare the existence or risk the penalty!

Moving on to the other ‘hot topic’ of the day ……… I am already hearing about lots of people who are being cold-called about the UK pension reform. Apparently, these calls are being made by people operating from Spain or Cyprus or perhaps some other place. Typically, they are offering to liberate your UK pension plans now. What do these people know about the French tax system and the implications for you? For that matter, do they even understand the UK tax implications for you?

Rob and I have both written articles on this subject and I hope that we are sending out a strong message of the need to exercise caution. Every case will need to be considered on its own merits – there will be no ‘one size fits all’. Anyway being able to cash in large pension pots is only a proposal at the moment. We will have to wait for the result of the consultation and then probably a few months more to know the outcome. So if you get any of those calls coming from outside of France, my advice is to tell them not to waste your time!

The final thing that I want to mention is our client seminars – Le Tour de Finance. This is a tour that travels around France, where we bring ‘experts to expats’ and we are now taking bookings for the Spring tour for which there will be presentations on the following subjects:

- Assurance Vie (two of our favoured providers will be presenting)

- QROPS & Pension Investing (very topical)

- Currency Exchange (is this a good time to exchange Sterling to Euros?)

- Health Insurance (are you affected if the UK stop issuing S1s to early retirees?)

- Wills in France & UK (are you affected by the EU succession rules from 2015?)

- International Banking (do your current bankers meet your needs?)

- Tax Advice in France (do you need help with those tax returns?)

Spectrum advisers will also be on hand at all events to answer questions. Maybe you need to have a more in-depth review of your financial situation. If so, we can arrange this with you.

As always, there is no charge for any of our seminars and the speakers’ presentations are followed by a buffet lunch/refreshments. The dates for the local events are:

- 21st May – Hotel La Villa Duflot, 66000 Perpignan

- 21st May – Hotel Abbaye École de Sorèze, 81540 Sorèze

- 22nd May – Côté Mas, 34530 Montagnac

- 23rd May – Montpellier Massane Golf & Spa Hotel, 34670 Baillargues

Each event starts at 10.00 am with a welcome coffee and ends at 2.00 pm after a buffet lunch, with the exception of Sorèze, which starts at 5.30 pm, finishes at 9.00 pm and refreshments will be served. The seminars are always very popular and so early booking is recommended.

If you would like to attend one of the seminars or you would like to have a confidential discussion on your financial situation, please contact me by telephone on 04 68 20 30 17 or by e-mail at daphne.foulkes@spectrum-ifa.com.

The above outline is provided for information purposes only and does not constitute advice or a recommendation from The Spectrum IFA Group to take any particular action on the subject of investment of financial assets or the mitigation of taxes.

Why expats should be wary of new pension rules

By Spectrum IFA

This article is published on: 16th April 2014

There are tax implications for Britons overseas who choose to cash in their pension money under new rules announced in the Budget.

British expatriates with UK pension pots who believe they can cash them in tax free from next April are in for a disappointment, according to pension experts.

Rob Hesketh from The Spectrum IFA Group comments in a case study within this Telegraph Newspaper article, please click here to read more

How can I find out more about the financial services that are available to me in France?

By Amanda Johnson

This article is published on: 15th April 2014

For the past few years in addition to running financial surgeries, where people can pop in & ask me questions they may have, The Spectrum IFA Group have also held tremendously successful “Tour de Finance” roadshows in the area in conjunction with Currencies Direct.

This year we will be at the beautiful Chateau de Saint Loup, in Saint Loup sur Thouet on Tuesday 17th June & our aim is to provide you with the opportunity to listen to various market leaders & complimentary service providers you may not have access to directly and informally, over a buffet lunch after, ask any questions you may have regarding your personal situation.

In addition to Currencies Direct and The Spectrum IFA Group we will be joined by a number of financial institutions including Prudential International, SEB & Standard Bank, as well as Chartered Accountants & international tax experts, PetersonSimms and experts in the French health system, Exclusive.

Starting with registration over coffee at 09.30 followed by a series of brief presentations and then a buffet lunch after, we plan to finish at around 14.30. Once the event is over you will be able to enjoy walking in the grounds of this lovely chateau.

Whether you want to register for our Tour de Finance road show, receive our regular newsletter or speak to me directly, please call or email me on the contacts below & I will be glad to help you. We do not charge for reviews, reports or recommendations we provide.

For more information on Le Tour de Finance please click here