Geopolitics and Oil Prices

Over the past couple of weeks I’ve received a number of questions from concerned clients about the latest geopolitical developments and what they might mean for markets.

Tel: +34 93 665 8596 |

info@spectrum-ifa.com |

![]()

By Peter Brooke

This article is published on: 14th March 2026

Over the past couple of weeks I’ve received a number of questions from concerned clients about the latest geopolitical developments and what they might mean for markets.

Whenever headlines become intense, it can understandably feel as though something dramatic must be happening in financial markets as well. The reality is often more nuanced — and this appears to be one of those moments.

Markets have reacted to rising geopolitical tensions, but the moves so far suggest caution rather than panic.

The key variable investors are watching is energy prices. Historically, bear markets tend to be linked to recessions, and the main risk from the current conflict is whether sustained oil price increases could slow economic growth.

Recent tensions in the Middle East involving Iran, the United States and Israel have dominated global headlines and created understandable concern among investors.

When events escalate quickly, it is easy to assume markets will react dramatically. Yet the response from investors so far has been far more measured. Markets have certainly moved, but the behaviour looks much more like caution than panic.

The real question investors are asking is not simply what is happening geopolitically — but whether it could become an economic shock.

So far, markets appear to be adjusting to geopolitical risk rather than assuming it will derail the global economy.

The most immediate reaction has been in energy markets.

Oil prices briefly surged as investors priced in the risk of supply disruption through the Strait of Hormuz, one of the most important shipping routes in the global energy system. At one stage prices approached $120 per barrel, before retreating to below $90, still significantly higher than the $65 level seen at the end of February.

This sensitivity reflects the strategic importance of the region. Roughly 20% of global oil supply normally passes through the Strait of Hormuz, meaning even temporary disruption can move prices quickly.

Equity markets have moved lower, although declines have been relatively contained. Across developed markets, equities have generally fallen between 2% and 6%, while emerging markets have seen slightly larger pullbacks due to their greater reliance on imported energy.

Safe-haven assets have also seen some demand. The US dollar strengthened, while gold briefly rose above $5,400 per ounce before easing again.

Despite dramatic headlines, the overall reaction has remained relatively orderly. As LGT Wealth Management noted in a recent update:

“While the headlines have been dramatic, market moves so far suggest investors are reacting with caution rather than panic.”

Interestingly, much of the volatility has occurred beneath the surface of markets. The Rathbones multi-asset team recently highlighted that while headline equity indices have only fallen around 3–4%, there has been significant rotation between sectors and individual stocks.

Chris Saunders of New Horizon Asset Management also notes that the conflict is beginning to affect other parts of the global economy. Disruptions to Iranian production have tightened fertiliser markets, pushing prices higher and raising the possibility that food prices could also rise in the months ahead.

When geopolitical crises occur, investors tend to focus on one key question: Could this trigger a recession?

This distinction is important because historically bear markets (defined as a fall of 20% or more in stock markets) tend to occur when the economy enters a recession, rather than simply because geopolitical tensions increase.

One of the main channels through which geopolitical events can affect economic growth is energy prices. Economists often use a simple rule of thumb: every $10 increase in oil prices can add roughly 0.3% to inflation and reduce economic growth by a similar amount.

With current expectations for US economic growth around 2.2%, oil prices would likely need to rise well above $120–$130 per barrel and remain there for a sustained period before recession risks became materially elevated.

At present, prices remain below those levels.

However, as Chris Saunders notes, the key variable may be how long the conflict continues, as prolonged disruption to Middle Eastern energy supply could delay interest-rate cuts and keep inflation pressures elevated.

This helps explain why markets have responded cautiously rather than dramatically.

Periods of geopolitical tension can certainly create short-term volatility, but they rarely change the long-term trajectory of global markets unless they spill over into the broader economy.

Portfolio managers also emphasise the importance of remaining disciplined during periods like this.

As one Rathbones portfolio manager noted in a recent discussion:

“What was a good company before the weekend is still a good company afterwards. The share price may now be lower — which can create opportunities.”

Similarly, the investment team at Atomos emphasised that predicting short-term market movements during geopolitical crises is extremely difficult, reinforcing the importance of maintaining diversified portfolios designed to withstand periods of uncertainty.

Energy shocks can also accelerate structural change. Previous crises — including Europe’s energy shock following Russia’s invasion of Ukraine — helped accelerate investment in renewable energy, batteries and alternative energy systems.

• Markets have reacted with caution rather than panic despite dramatic geopolitical headlines

• Oil prices remain the key variable investors are watching

• Historically, bear markets are far more closely linked to recessions than geopolitical events alone

• Current oil prices remain below levels historically associated with recession risk

• Maintaining a disciplined, diversified investment strategy remains the most effective approach during volatility

Geopolitical developments will inevitably continue to evolve over the coming weeks. However, markets so far appear to be adjusting rather than overreacting.

History repeatedly shows that while headlines can move quickly, markets often prove more resilient than expected.

I hope you found this update interesting and helpful.

If anything has raised questions for you, or you’d simply like to talk something through, please don’t hesitate to get in touch. That’s exactly what I’m here for.

Please complete the form below:

By Peter Brooke

This article is published on: 12th March 2026

I hope this newsletter finds you well; So, pensions are back in the spotlight as governments in the UK and Ireland introduce meaningful changes that could affect how individuals and business owners save for retirement. In this edition, we break down what’s changing, why it matters, and what you should be thinking about next.

As you may have seen in the recent UK budget from April 2026, most expatriates will no longer be eligible to pay Class 2 National Insurance Contributions (NICs) and will instead need to use Class 3 contributions which cost more — but this still may offer an excellent return on investment.

The ruling states:

“From 6 April 2026, individuals will no longer be able to pay voluntary Class 2 NICs for periods abroad. Only voluntary Class 3 contributions will be available for tax years 2026 to 2027 onwards.

This change does not affect any voluntary contributions that can be paid for periods abroad before 6 April 2026 – there is more detail here

If you’d like help interpreting your forecast or reviewing your eligibility for Class 2 vs Class 3 contributions, feel free to share the summary or screenshots — I’ll walk you through the options.

The ruling also states that “New applications to pay voluntary Class 3 NICs will need to have either”

What remains unclear is whether contributions paid for whilst abroad will count towards the 10 year rule and whether it is therefore sensible to pay for missing years before April 2026 to ensure you have 10 qualifying years so that you will be eligible to pay future years.

It certainly appears that long term non-UK residents, without 10 years of NICs, could be “locked out” of the system from April.

Based on current UK State Pension levels, even at Class 3 NIC rates (around £900 per year), each extra qualifying year typically adds about £330 per year to your State Pension for life (though this will depend on future government policy).

This means most people recover the cost in less than three years of receiving their pension — and every year after that is a financial gain.

You generally need 35 qualifying years of National Insurance contributions to receive the full UK State Pension. That’s why it’s important to know three things:

Once you understand these three numbers, you can work out exactly how many additional years you might need. And remember: you may not have to pay for every remaining year at the higher Class 3 rate after April 2026.

Many expatriates will reach the 35-year mark using a combination of existing contributions, cheaper buy-back years, and only a small number of future payments.

Government Gateway tip:

To log in, you need to receive a security code by text message. If you change your mobile number, make sure you update it with HMRC before you lose access to the old phone number. Otherwise, you may be locked out of your Government Gateway account and unable to view your State Pension record.

Ireland is restructuring older Executive Pension Plans (EPPs), and by April 2026 the IORP II regulations (see details here) will require EPP schemes to either:

…or risk becoming frozen or facing significantly higher running costs.

For clients living outside Ireland, the decision between these options is particularly important.

If you expect to remain an EU resident during retirement, there are often strong long-term reasons to transfer your pension out of Ireland; (I cant cover this in this newsletter but contact me if you want more information).

Because of this, it is crucial that whatever happens to your pension today does not restrict your ability to make that transfer in the future.

To protect your future options, we strongly recommend:

✔ Before agreeing to a Master Trust transfer, obtain written confirmation that the scheme allows transfers to foreign pension arrangements in the future.

✔ Do not sign any PRSA transfer paperwork without a full review of the long-term implications.

✔ Forward any pension documents or transfer requests to us — we will assess them for you and advise on your position.

We help clients:

If you hold — or think you may hold — an Irish Executive Pension, reply to this email or click here to schedule a consultation.

We’ll ensure the restructuring supports your long-term financial interests, rather than simply following administrative defaults.

Since Brexit, many expatriates are discovering that once they are no longer UK-resident, it is often not possible to receive ongoing regulated advice on their UK pensions from either UK-based advisers or overseas firms like Spectrum.

We regularly see clients being contacted by their UK adviser or pension provider and told that the relationship must end — leaving them unadvised and unable to manage their pensions effectively.

At the same time, changes to pension regulation mean that QROPS transfers are now far less common and often no longer suitable. This leaves many expatriates unsure how to handle their UK pension schemes as they approach or move through retirement.

Your UK pensions can still be actively and professionally managed by a local adviser by transferring them to an International SIPP. This can also allow you to consolidate multiple pension pots into one, making your retirement planning far simpler.

An International SIPP can provide:

✔ Access to regulated advice

✔ Better consolidation and control, including currency options

✔ Potentially lower fees

✔ A flexible investment approach aligned to your residency and long-term goals

We can help you:

You don’t need to leave your pension un-managed. Send us your pension information and we’ll assess whether an International SIPP could allow us to advise you properly and optimise your retirement planning.

Important pension changes are now underway across the UK and Ireland and for many expatriates and business owners these changes create both risk and opportunity.

Across all three areas, the key message is the same: early decisions have long-term consequences. A short review today can protect flexibility, reduce future costs, and strengthen your retirement position.

If any of these changes affect you, we encourage you to get in touch. We’re here to help you navigate the complexity and ensure your pension remains aligned with your long-term plans.

If you have any questions please send them via the channels below, or the booking system – always drop me a quick message if you need a time slot outside of those available.

If you have missed any previous emails, click here to access the Archive.

For now, have a great day, speak soon…

Best regards

Peter Brooke

Mobile & Whatsapp: +33 6 87 13 68 71

Email: peter.brooke@spectrum-ifa.com

Calendly booking system: https://calendly.com/peterbrooke/30min

By Peter Brooke

This article is published on: 9th February 2026

I’ve just returned from the 23rd Spectrum annual conference — my 22nd — which this year was held in Monaco, making it refreshingly easy travel for me.

Each year we bring together Spectrum advisers from across Europe, along with our support and management teams, and a carefully chosen group of investment managers, pension specialists, and tax experts. It’s a chance to step away from the day-to-day detail, compare notes, challenge assumptions, and make sure the advice we give clients continues to stand up in a changing world.

One thing that’s worth sharing, because it underpins everything else in this update, is what Spectrum actually is. We’re a large, international advisory firm — but we’re also owned by the advisers who work in it. We’re currently restructuring the business to widen that ownership further, so more advisers have a direct stake in the firm’s future.

That matters because we’re not building towards a quick exit. We’re building something designed to last, we are proud of the longevity of the business and the strong retention of our advice team. The conversations at the conference reflected that long-term mindset — less about chasing the next headline, and more about understanding the forces that genuinely shape investment outcomes over time.

With that in mind, here are the main themes I took away from the conference, and why they matter for expatriates and internationally mobile families.

Artificial intelligence was easily the dominant topic of the conference — but not in the “buzzword of the month” sense. The most interesting discussions weren’t about which stock has run the hardest, but about where AI is genuinely changing productivity, margins, and long-term business models.

The key message from managers like Rathbones and Evelyn Partners was that we’re moving into a second phase of the AI story. The early gains were very concentrated — a small group of large US technology companies driving market returns. That phase isn’t necessarily over, but it is evolving.

What’s happening now is a broadening out. AI is starting to affect industrial businesses, healthcare, logistics, energy management, data infrastructure, and even areas like waste management and defence. In other words, it’s moving from “who builds the chips” to “who uses the technology well”.

That distinction matters. History shows that transformative technologies don’t just reward the obvious early winners — they reward companies that apply them intelligently, efficiently, and profitably. For investors, this reinforces the importance of looking beyond the headlines and staying diversified, rather than assuming yesterday’s winners will automatically dominate tomorrow as well.

Another strong theme that came through very clearly was a return to fundamentals.

Markets over the last couple of years have often felt narrow and momentum-driven, with a small number of stocks (mainly AI/Tech) doing most of the work. Several managers made the point that this sort of environment can feel exciting — but it also increases risk if portfolios become too concentrated – at one point just 7 companies made up nearly 35% of the size of the US stock market (S&P 500)!

Rather than trying to predict short-term market moves, the emphasis is now firmly back on:

cash flow and balance sheet strength

sensible valuations

real earnings growth

businesses with pricing power and durable demand

For clients, this translates into something reassuringly familiar: diversification still matters. Not just across regions, but across styles, sectors, and asset classes. It’s rarely the most exciting message — but it’s consistently one of the most effective.

Several presentations also focused on areas outside traditional listed markets.

There was strong interest in private assets and real assets — things like infrastructure, property, and long-term income-producing investments. These aren’t about quick wins; they’re about accessing different return drivers and reducing reliance on public market volatility alone.

For many expatriate investors, this can be particularly valuable. Income that’s less sensitive to daily market swings, assets linked to real economic activity, and structures designed with long-term planning in mind can all play a role alongside more traditional portfolios.

As always, these areas need careful selection and suitability — but the message was clear: a well-built portfolio doesn’t rely on a single engine to get where it’s going.

Another interesting thread was the importance of scale and governance, particularly in uncertain markets.

From an investment perspective, larger, well-capitalised businesses tend to have more resilience: better access to finance, more flexibility in downturns, and greater ability to invest through cycles rather than cut back at the wrong time.

That same principle applies at an advisory level too. Spectrum’s size, international reach, and shared ownership model allow us to invest in systems, compliance, and expertise in a way that simply isn’t possible for smaller, standalone firms.

It’s not about being big for the sake of it — it’s about stability, continuity, and quality of advice over decades, not just years.

Another reassuring takeaway from conference was spending time with the firms we work with on clients’ behalf — not just listening to presentations, but understanding how they think, how they’re governed, and how decisions actually get made.

One of the advantages of being part of a group like Spectrum is that we’re able to be selective. We don’t work with managers because they’re fashionable or because they shout the loudest — we work with them because they have depth, longevity, and a track record of navigating change.

None of this guarantees outcomes — nothing ever does — but it does give us confidence. These are organisations built to endure, with governance structures and cultures that align closely with how we think about long-term planning for clients.

For me, this is a crucial but often invisible part of the job: doing the work behind the scenes so that clients don’t need to worry about whether the foundations are solid. The conference reinforced that the partners we choose, and the effort that goes into maintaining those relationships, genuinely matters.

Stepping back, the conference reinforced something I see year after year: successful long-term investing is rarely about prediction.

It’s about:

That’s particularly important for expatriates, where cross-border rules, currencies, tax systems, and future uncertainty add extra layers to every decision.

If you’d like to talk through how these themes relate to your own situation — or simply want a sense-check that your plans still reflect what matters most to you — that’s exactly what I’m here for.

If you want to dive a little deeper into any of this detail, there are some great articles at these links.

Evelyn Partners Turning data into dollars in 2026

Rathbones Video Market broadening and Geopolitical noise

If you feel this would be helpful to friends, family or colleagues, please do feel free to forward this on to them.

As always, I’ll keep translating what we hear from conferences like this into practical, real-world advice that fits your life, not just the markets.

Finally, I’d like to say a genuine thank you to the firms who took the time to join us in Monaco, share their thinking so openly, and engage in thoughtful, sometimes challenging discussion.

In particular, my thanks go to the teams from Rathbones Asset Management, Evelyn Partners, LGT Wealth Management, Alquity VAM Investment Management, New Horizon Asset Management and Prudential International, and the other investment, pension, and tax specialists who contributed to the conference.

These events only work because people are willing to go beyond polished presentations and talk honestly about risks, opportunities, and uncertainties. That openness is exactly what helps us refine our thinking and, ultimately, improve the advice we give to clients.

It was a privilege to spend time with such high-quality partners — and it left me confident not only in the ideas discussed, but in the people and organisations helping us put those ideas into practice.

By Peter Brooke

This article is published on: 25th December 2025

As we come to the end of the year, we wanted to share a brief reflection on what has been a challenging but ultimately rewarding period for investors.

It’s been another unusual year (I think I wrote that in my last Christmas newsletter!!). We began 2025 with talk of a Trump tariff driven recession, interest rate cuts and the end of US dollar dominance. Instead, growth has slowed but not collapsed, interest rates have stayed higher for longer, and after weakening early in the year, the US dollar has strengthened again in the second half of 2025.

Equities experienced volatility along the way, driven by geopolitics, policy changes and concerns around inflation. Despite this, strong company earnings — particularly in technology and AI — helped global markets finish the year close to record highs. This was a reminder of the value of staying invested through short-term uncertainty.

Bonds quietly did their job. While yields rose earlier in the year, they provided attractive income and stability, reinforcing their role as a key diversifier within portfolios.

Gold stood out as a strong performer, offering effective protection against geopolitical and economic uncertainty while contributing positively to returns.

Overall, 2025 reinforced an important lesson: diversified, multi-asset portfolios can help investors navigate uncertainty and capture long-term opportunities — even in unsettled markets.

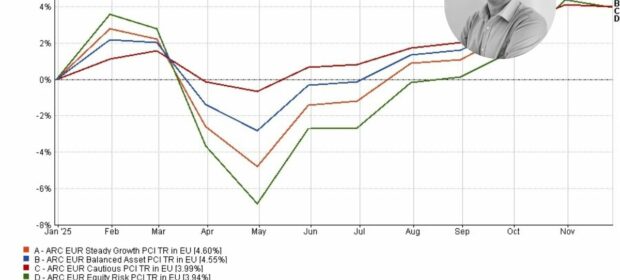

You’ll see below a chart showing the ARC Euro Indices for this year; the movements reflect the periods of volatility investors experienced, especially post ‘Liberation Day’ followed by a recovery as confidence improved.

It’s a helpful visual reminder that while markets rarely move in a straight line, staying invested through the ups and downs has historically been key to achieving long-term outcomes.

As we head into the festive season, I’d like to thank you for your continued trust and wish you and your family a very happy Christmas and a healthy, prosperous New Year.

I will be back in touch in January with a financial outlook for 2026 following our next annual Spectrum conference and, of course, I plan to continue to provide you with updates, developments and new support tools over the year ahead…

By Peter Brooke

This article is published on: 6th September 2025

Karen Tait – Host and Presenter

Lisa Greene – French property expert (LEGGETT Immobilier Intl)

Jonathan Watson – Currency Specialist (LUMON)

Paulette Booth – Insurance expert (AXA International)

Tracy Leonetti – Relocation & French admin expert (LBS in France)

Sharon Revol – Mortgage expert (Cafpi)

Peter Brooke – Tax and Wealth Expert (The Spectrum IFA Group)

Speak to the experts about the property buying process in France, currencies transactions, insurance, the relocation paperwork…, mortgages in France, plus the all important financial and tax questions about moving to France.

Sign-up to the webinar – and if you have some specific questions, enter them on the form and our panel of experts will do their very best to answer your questions during the webinar on Wednesday 24th September

By Peter Brooke

This article is published on: 30th May 2025

I recently attended the FEIFA Annual Adviser Conference in London and wanted to share a brief summary of the latest market insights, along with how advisers are continuing to evolve their approach to best serve clients in today’s environment.

The Federation of European Independent Financial Advisers (FEIFA) – not to be confused with the football governing body! – was founded 16 years ago by a group of experienced IFA firms across Europe. They saw the need for an organisation that could uphold professional standards and represent the interests of advisers and their clients with both industry bodies and regulators across the continent. Spectrum is proud to be one of the original founding members, and we continue to support and build on those standards through our ongoing involvement.

The annual conference brings together FEIFA members and leading industry voices to discuss the unique challenges of advising cross-border clients. As Head of the Spectrum Investment Committee, it remains a valuable and important event in my calendar.

Staying the Course Through Market Volatility

Richard Flood (RBC Brewin Dolphin) reminded us that global events—whether pandemics, wars, or political wrangling —are a constant. Despite this, markets rise over time. The key is to focus on long-term fundamentals rather than react to short-term noise.

Volatility, he stressed, is a normal part of investing and “the price you pay for superior returns.”

Avoiding volatility by sitting in cash is not a good idea either as Inflation diminishes the purchasing power of cash – as illustrated in this Equities v’s Cash ‘inflation adjusted’ performance chart.

Navigating an Uncertain 2025

David Coombs (Rathbones) highlighted the ongoing impact of geopolitical events like Trump’s executive orders and Tariffs on trade and compared them to other countries ‘protectionist policies’ like unbalanced tax rates (eg Ireland), agricultural subsidies (eg France).

He also stressed the unconsidered challenges that passive investments (eg ETFs) pose to market stability due to being “forced sellers & and forced buyers” therefore adding to volatility.

Active management, in his view, remains vital, especially in 2025, and he shared a wonderful example of how active he has been in the last year:

The below chart is the Shopify share price, a share he has held for some time, the red dots are where he sold some shares (trimmed) and the yellow dots are where he added money – this shows that active management is much more than strategically choosing which companies to own or not own, but how to add value through tactical decisions.

The Passive Investing Paradox

Henry Wilson (LGT Wealth Management) discussed the risks of over-reliance on passive funds, including the concentration risk in a few large companies (eg MAG 7). Because of this concentration of returns (and risk) to fewer, larger companies he believes that true diversification is under threat, valuations are higher, future returns are compromised…

… BUT as Harry Markowitz, the architect of Modern Portfolio Theory & Efficient Frontier said “Diversification is the only free lunch to investing”.

Therefore while passive investing remains a useful tool, LGT and Spectrum advocate for highly diversified, actively managed portfolios to help manage risk and improve long-term returns.

If you are going to own passive investments you have to be active with them.

Model Portfolios & Adviser Alpha

Matthew Lamb (Pacific Asset Management) explored the evolution of model portfolios and the increasing role of technology. With many portfolios becoming similar, the real value lies in the advice given—not just the investments chosen.

This fits strongly with my recent newsletter about risk (click here) – If most ‘Balanced’ portfolios are similar to each other and most ‘Growth’ portfolios are similar to each other then the outcome for you, as my client, is not in picking between two balanced funds or two growth funds… it’s ensuring we choose correctly between Balanced or Growth in the first place!!

Good risk profiling conversations make sure we start in the right place.

Planning for the Summer

After almost 13 years, we’re finally heading to Australia for a long-overdue family holiday. We’ll be visiting my wife’s side of the family, who all live in Queensland. She’s been able to make a few trips in that time, but between school schedules, travel costs and a global pandemic, the children and I haven’t been back since 2013. We’ll be away for five weeks from the end of June and are really looking forward to the trip.

I’ll still be checking emails and messages periodically, but if you’d like to catch up — whether by phone, Zoom or in person before we go — please do get in touch or book something in the calendar before Friday 27th June.

All being well, I’ll be back at my desk (with a fair dose of jet lag) on Wednesday 6th August.

Lions V’s Australia

Of course, seeing family and friends is the main priority — but I’d be lying if I said there wasn’t something else I’m particularly excited about.

As a lifelong rugby fan, getting the chance to see the British & Irish Lions take on Australia in both the 1st and 3rd Test Matches — plus the Queensland Reds in early July — is nothing short of a bucket list experience for me.

As always, if there’s anything you’d like to go over before I head off, just let me know. And if anything comes up while I’m away, I’ll do my best to ensure it’s handled smoothly.

Contact me if you have any questions via the below channels, or the booking system – always drop me a quick message if you need a time slot outside of those available.

Mobile & Whatsapp: +33 6 87 13 68 71

Email: peter.brooke@spectrum-ifa.com

Calendly booking system: https://calendly.com/peterbrooke/30min

By Peter Brooke

This article is published on: 8th April 2025

Quite understandably my inbox has been full of messages from concerned clients and musings from commentators and investment managers about how to respond to the current market reaction to President Trump’s raft of tariffs.

The uncertainty around how these tariffs will play out has led to large falls in stock markets, especially the US.

As discussed in my last newsletter Lets Talk About Risk, volatility is an important and unavoidable part of investing and will be negated by time in the market and can provide great opportunities. The key is to ‘stay the course’ and try and ‘see through the noise’.

However, I did want to get something out to you with some current thoughts about what is happening, what might happen in the near future and why ‘staying the course’ is the best option.

When markets turn volatile, perspective is everything.

The past week feels pretty tumultuous but, of course, we’ve been here before.

The table below shows the maximum intra-year drawdowns (DD) and end-of-year total returns (TR) for the S&P 500 from 1950 to 2025.

It reveals that after severe drawdowns, the market has often recovered the full decline and finished the year strongly positive.

Years to Note:

On each occasion, the best course of action would have been to avoid the noise and stay invested.

I hope that the above shows that though periods of volatility will always happen and always be temporary it is best to stay the course and try and avoid the noise;

I do appreciate that it is difficult with today’s ‘news’ channels adding to the feeling of panic on an hourly basis so I have shared below some links from firms much closer to the markets to share more detail about what is happening and what investors should consider in these temporarily volatile times.

Traversing Trump tariffs by Daniel Casali, Chief Investment Strategist at Evelyn Partners

Trump’s tariffs: how should investors respond? From Rathbones Investment Management

I would like, once again, to thank these expert commentators and the team at New Horizon Asset Management for their quick and important updates to a challenging situation.

As always, please remember that financial decisions should be made with careful consideration of individual circumstances and professional advice, I am here to support you.

If you have missed any previous news and updates these can all be found on the archive page here.

If you have any questions please use the the below channels, or the booking system – always drop me a quick message if you need a time slot outside of those available.

Mobile & Whatsapp: +33 6 87 13 68 71

Email: peter.brooke@spectrum-ifa.com

Facebook: Peter Brooke – Financial Advice

Calendly: https://calendly.com/peterbrooke/30min

By Peter Brooke

This article is published on: 30th March 2025

“Risk” is an unavoidable, and sometimes welcome, part of investing so having a better understanding of the different forms of risk can help investors make informed decisions that align with their financial goals. In this (quite long) article, we explore key types of “risks” and how they impact financial planning.

Definition: The possibility of something bad happening!!

Definition: The degree of uncertainty and/or potential financial loss inherent in an investment decision.

So we need to frame our conversations about “RISK” by trying to understand the ‘something bad’ in every decision we make.

Inflation Risk: The risk of doing nothing!

A.K.A. – The Erosion of Purchasing Power

Inflation risk occurs when the value of money declines over time, reducing its purchasing power.

For example, if inflation averages 2.5% per year, €100 will only buy €53.10 of goods in 25 years’ time.

To counteract inflation risk, investors should turn to non-cash assets like shares and bonds, which have historically always outpaced inflation over the long term.

What’s the something bad? – The risk of doing nothing and leaving money in a bank account will guarantee a financial loss over the long term.

Permanent and Total Loss of Capital

Companies can and do ‘go bust’ and for an investor in those company’s shares this would mean a total and permanent loss of capital – the share price falling to zero.

Therefore understanding how a company is managed and investing across a diversified group of high quality companies will minimise this risk.

Outsourcing to a fund manager to diversify this risk is a great way to ‘avoid the losers’ even if you don’t always ‘own all the winners’.

What’s the something bad? – Investing in just one or a few companies and not understanding the ‘fundamentals’ of each investment.

Volatility: Fluctuations in Values

Volatility is often ‘defined’ as RISK with respect to investments.

Volatility refers to short-term fluctuations in the price of an investment; for example a share price.

While dramatic drops can be unsettling, history shows that volatility is entirely normal and markets always recover over time.

For example, look at the chart below; since 1980, the US stock market (S&P 500) has experienced declines averaging 14.1% during each year, yet annual returns were positive in 34 of those 45 years (75%).

The red figures show the largest market drop in value for each year and the grey bars show the total return for that same year… for example 2024 shows a drawdown of 8% but the S&P 500 finished the year 23% up.

Volatility is NORMAL and does NOT mean a capital loss for the long term investor.

Volatility risk is mitigated by TIME in the market

Volatility is part and parcel of investing, and your investment time horizon almost without exception determines the likelihood of investment success. This chart shows the annualised returns over four different time frames (1, 5, 10 and 20 years) using data from 1950 to today.

A 50/50 portfolio of shares and bonds (the green bar) shows that in the last 75 years you could lose up to 24% or gain up to 49% in any given one year period.

However, over every 10 year rolling period in that same 75 years, your worst possible return would be 1% p.a, (ie. no loss) and the best would be 17% p.a.

The longer the investment term, the less relevant volatility becomes, and crucially, the longer the investment term, the greater the likelihood of investment success.

What’s the something bad? – Not maintaining a long-term perspective and reacting impulsively to market swings.

Longevity Risk: Outliving Your Wealth

With increasing life expectancy, investors must consider the risk of outliving their assets.

For a couple aged 65 today there is a 92% chance that one of them will live to 80 and a 49% chance one will live to 90.

Planning for a longer retirement by investing must now include more exposure to growth-oriented assets.

Sequencing Risk/ The Timing of Returns Matters

For retirees or those drawing an income from investments, sequencing risk— the order in which returns occur— can significantly impact portfolio longevity.

A market downturn early in retirement can lead to a faster depletion of funds compared to a downturn later in retirement.

Strategies like maintaining a cash reserve, actively managing portfolio risk as you approach retirement and diversifying investment assets will help.

What’s the something bad? – A market correction just at the point of retirement can significantly impact the quality of that retirement.

ROMO – The Risk Of Missing Out: The Cost of Not Investing

As well as the risk of not keeping up with inflation, there is also a significant risk (and great financial cost) in staying out of the market.

The ‘magic of compounding’ delivers substantial rewards for the patient, long term investor.

The 8 – 4 – 3 Rule

Here is a table showing the compounding effect of a 7% annual return:

What’s the something bad? – The risk of doing nothing and not benefiting from compounding returns.

Currency Risk

Expatriates often have assets in one currency but expenditure in another; for example a Pension in British Pounds and outgoings in Euros.

As global investors there will always be some form of underlying currency risk but mitigating the practicalities of moving money around from one currency to another is possible with careful planning.

Options could be:

What’s the something bad? – The risk of not correctly matching your assets with your liabilities – a large fluctuation affects your lifestyle.

Assessing Your Attitude to Risk:

All of the above is to help our conversation about ‘RISK’ but in order to best set up and review your investment portfolio we have a 3 part process to determine exactly how much investment risk you can tolerate:

1. Your ATTITUDE to risk – this is a psychometric test, via a questionnaire, to assess your in-built view on risks, volatility and returns.

2. Your CAPACITY to take risk – this is a deeper understanding of your overall situation and therefore your ability to weather ups and downs in portfolio values… i.e. do you have other assets, a large pension or property income; how reliant are you on your portfolio at any given time?

3. Your TIME HORIZON for investing – when do you need to access to this money? Will the access be to draw an income or large lump sums or even, all of the fund in one go? Or is this money just to be invested to pass on to beneficiaries?

The answers to these 3 questions provide us with a ‘score’ and ‘understanding’ of how you will use the money being invested… this allows us to assign a ‘Risk Benchmark’ to your portfolio, from which we will determine its asset allocation and then monitor its performance and volatility for the duration of the investment.

Obviously, your TIMESCALE changes over time and your CAPACITY can change as your life situation changes; even if you maintain the same inherent ATTITUDE to risk we must always review and monitor the overall position of your portfolio and potentially change your benchmark as time passes.

Final Thoughts

Investing always carries ‘risks’, but knowledge and strategy can help manage them effectively. Whether it’s inflation, market fluctuations, or longevity concerns, working with a financial adviser ensures that risk is considered within a well-thought-out plan. Overall doing nothing is the largest risk.

Staying focused on long-term goals, and avoiding emotional reactions to short-term market movements, usually leads to successful financial outcomes.

I would very much like to thank the team at RBC Brewin Dolphin for their kind input and help with this article, I truly hope you found it useful.

If you’d like to discuss your investment strategy and how to manage these risks, feel free to get in touch!

By Peter Brooke

This article is published on: 7th March 2025

I’m always looking for ways to improve how we can work together, ensuring that your financial planning experience is seamless, efficient, and tailored to your needs. To that end, I am excited to share some recent technology updates that will enhance our communication and collaboration.

These two new enhancements add to the suite of tech tools I am already using to save time, improve communication, improve my efficiency in dealing with follow up tasks and provide you with the best financial planning service possible.

Spectrum advisers and our clients are spread across Europe and so we have invested into an innovative virtual office via App.Spatial.chat to offer a more interactive and engaging way to meet remotely. This platform allows for an easy to use virtual face-to-face experience, making it easier for us to discuss your financial plans in a comfortable, secure setting – whether you’re at home or on the go.

This tech does not replace face-to-face meetings but offers us another way of meeting. I will be offering this as an invite option via my Calendly Booking system as well as zoom, teams, telephone calls and, of course, face to face meetings.

When you enter the Spectrum Virtual office, as a guest, you will see a brief introduction as to how it works, you can then enter the main office or any of our ‘country’ offices, via the list on the right hand side of the screen.

Our meetings will be conducted in my own personal office which is password protected so we have complete privacy from anyone else who might be online at the time.

I look forward to seeing some of you there over the coming months.

To ensure I capture every important detail during our discussions, I will now be using Otter.ai to record virtual and even live face to face meetings, with the agreement of my clients.

This tool allows me to create accurate transcripts of our conversations, helping me stay fully aligned with your financial goals and ensuring that nothing is overlooked.

Rest assured, all recordings and transcriptions will be handled securely, I permanently delete each one as soon as I have downloaded the transcribed notes and follow up to task lists, maintaining strict confidentiality in accordance with data protection standards.

Click on the following image to view a brief introduction to Otter

If you prefer for me not to record our meetings, please say so, and I will turn off the tech. Likewise, if you want me to send you the notes I would be very happy to.

Cash Calc Secure Client Portal for data gathering, expense tracking, document sharing and even secure messaging: https://the-spectrum-ifa-group-1002.cashcalc.co.uk/register?ref=MTIzMTU=

Calendly booking system for easy call and meeting booking linked straight to my diary https://calendly.com/peterbrooke/30min

DocuSign and Adobe Sign – these allow me to send you paperwork to sign digitally and securely to save us all time and the requirement to print and post documents.

The future of finance is undeniably tech-enabled. By embracing AI and support tools like these, we plan to remain competitive, agile, and customer-focused.

Feel free to get in touch if you have any questions via the below channels, or the booking system – always drop me a quick message if you need a time slot outside of those available.

If you have missed any previous emails, click here to access the Archive.

For now, have a great day, speak soon…

By Peter Brooke

This article is published on: 4th February 2025

Looking forward to 2025

Another year and another wonderful Spectrum conference. More on that in a moment.

Last year, in Budapest, was my 20th conference with Spectrum after which I offered a fairly cautious outlook for the year to come. You can review my thoughts in The view from the Danube

I have now just returned from a superb four days in Casablanca, hence the name of this piece, which was our first ever conference outside of Europe. We had another great group of experts who shared their views on the key themes likely to shape 2025. From the future of US markets under Trump 2.0 to opportunities in bonds and the transformative power of AI; here’s a summary of the insights most relevant to your investments and financial goals. Overall I feel cautiously optimistic looking forward to 2025.

Even with the slightly pessimistic outlook for 2024, the US stock market had an exceptional year, with the S&P500 delivering one of its strongest performances in history, though much of this was led by a small handful of stocks.

As we look to 2025, several factors suggest US markets could remain a standout:

Momentum: The US economy grew by 3.2% in 2023 and is forecasted to grow 2.8% in 2024, showing resilience despite high inflation and interest rates.

Earnings Growth: US companies are projected to achieve earnings growth of 13.8% in 2025—significantly higher than the 7.4% forecast for European companies.

Profitability: The US has long maintained a profitability edge over other developed economies, and Trump’s deregulation efforts could further enhance competitiveness.

Structural Advantages: Energy independence, favourable demographics, and leadership in technology (particularly AI) continue to position the US ahead of its global peers.

With the Republican Party securing a clean sweep in the 2024 elections, President Trump is expected to have more freedom to implement his policies in his second term. Here’s what investors should consider:

Bonds are regaining their appeal:

Attractive Yields: UK gilts are offering a 5.5% yield, equivalent to a real return of nearly 3%, presenting an appealing alternative to equities, especially in Europe.

Diverse Opportunities: Investors are also finding value in international bonds, including those from Portugal, Romania, and Germany.

Volatility Awareness: Bonds have become as volatile as equities, underscoring the need for a well-diversified portfolio.

The AI revolution is driving innovation and creating new opportunities across industries. It is important to consider those companies who will be enabled by AI and who will earn from “enabling the enabled” as well as those companies supporting the infrastructure of AI.

Key investment areas include:

Data Ownership and Infrastructure: Companies like RELX (legal and medical data) and Equinix (data centres) are poised to benefit from the AI boom.

Efficiency Gains: Firms such as Rentokil and Waste Management are leveraging AI to optimise operations and drive growth.

Cloud Infrastructure: AI can’t happen without the Cloud.

Understanding and managing risk is critical to achieving long-term financial success. I will be writing a newsletter in the coming months focussing solely on ‘risk,’ but for now here are key considerations:

Inflation remains sticky: The risk of doing nothing could erode your cash’s value over time.

Volatility: Short-term market fluctuations are normal but tend to even out over time, emphasising the importance of staying invested.

Longevity: For couples, there’s a 50% chance one partner will live to age 90—making a long-term income strategy essential.

Sequencing Risk: Timing withdrawals during retirement requires careful planning to avoid depleting your assets prematurely.

With markets adapting to new norms, a balanced and diversified approach remains crucial:

US Market Focus: While US equities remain a core component, avoiding over-concentration in sectors like AI is vital. Just 7 companies make up 33% of the S&P 500 index and contributed 55% of all the returns of the S&P500 in 2024 – the largest concentration in history.

Employ Active Managers: Passive investors have had a great run, especially if invested in US equities but as we have already seen this month the AI Titans have sold off on one piece of news from China. Active managers will control these concentration risks.

Global Bonds: High yields make bonds an attractive addition to portfolios, particularly for those seeking income and stability.

Alternative Investments: Assets like gold can provide a hedge against geopolitical risks and inflation.

I would very much like to thank the investment management teams at RBC Brewin Dolphin, Rathbones Investment Management, Evelyn Partners, New Horizons, Alquity Investments, VAM Funds and Prudential International for their time and expert views for the content in this update.

Here are some links to other articles supporting this summary if you want to dive deeper into the details:

US Continues to Outperform https://www.evelyn.com/insights-and-events/insights/can-us-outperformance-continue/

A look back on 2024 https://www.evelyn.com/insights-and-events/insights/2024-investment-review-ifa/

Trump 2.0 https://www.lgtwm.com/uk-en/insights/market-views/trump-politics-the-global-order-250934

The excellent monthly Rathbones Sharpe End Podcast https://www.rathbonesam.com/uk/sharpe-end-podcast#podcasts